It Wasn't the Debt.

What the DSO lender takeovers actually revealed — and why the same failure is sitting inside your practice right now.

Kingsley Group — Institutional Analysis · July 2026

It Wasn't the Debt.

What the DSO lender takeovers actually revealed — and why the same failure is sitting inside your practice right now.

Kingsley Group — Institutional AnalysisIn the first half of 2026, two major dental support organizations in the United States reportedly passed into the control of their lenders following restructuring. Between them, they represent hundreds of supported locations and decades of accumulated acquisition.

The industry read it as an interest-rate story. Cheap debt fueled the roll-up era; expensive debt ended it. Clean narrative. Comfortable, too — because if the failure was macroeconomic, no one inside the buildings did anything wrong.

That reading does not survive contact with the rest of this year's data.

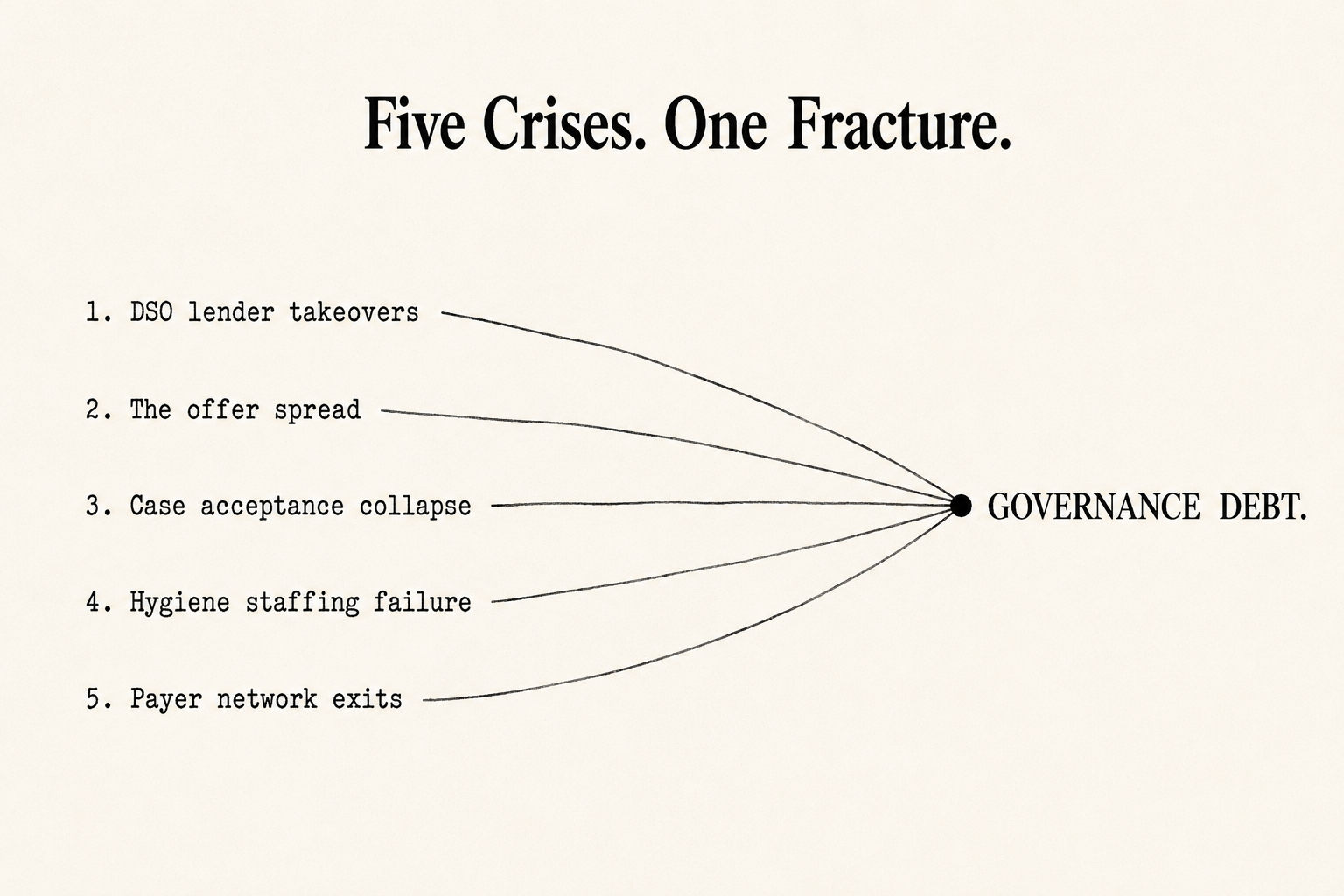

Five headlines, one variable.

Consider what else the trade press published in the same window.

The most-cited market report of the quarter found that the defining feature of dental M&A is no longer the multiple — it is the spread. Practices with comparable revenue, comparable payer mix, and comparable specialty are receiving offers turns apart. Buyers, 69% of whom intend to acquire more this year, are simultaneously applying unprecedented scrutiny to financials, operations, and performance projections before they transact.

Meanwhile: one-third of dentists report they are not busy enough. Barely 47% of recommended treatment is accepted. Ninety percent of owners describe hygiene recruiting as very or extremely challenging — and the sector's own salary data shows the problem is not purely wages. Nearly a third of dentists exited at least one insurance network last year, most making that decision practice by practice, informally, with no documented framework for what the decision obligates downstream.

And two platforms that had successfully executed the acquisition playbook for years lost control of their own companies.

The industry is treating these as five separate crises: a valuation problem, a demand problem, a staffing problem, a payer problem, and a leverage problem. They are not five problems. They are five surfaces of one structural condition.

Dentistry is misdiagnosing a governance crisis as everything else.

The condition, named

Every dental organization — from a two-operatory practice to a 300-location platform — runs on a set of answers to unglamorous questions. Who decides? Who owns the outcome when the decision fails? Where is the decision recorded? What happens when the person who "just knows" is unavailable, retires, sells, or quits?

When those answers live in individuals rather than in architecture, the organization is carrying what we term Governance Debt: the accumulated gap between the complexity an enterprise operates at and the decision systems it actually possesses. Like financial debt, it compounds quietly. Unlike financial debt, it does not appear on any statement — until an event forces it into the open.

2026 is the year the events arrived.

At the platform level, Governance Debt is what turns leverage fatal. Debt did not kill the failed DSOs; debt merely called the question. Organizations that acquired faster than they could integrate — where authority was ambiguous across regions, where clinical alignment was aspirational, where the operating infrastructure never caught up to the footprint — had no coherence to fall back on when margins compressed. Industry post-mortems have said as much: the survivors will be defined by operational infrastructure, clinical leadership, and doctor support, not by acquisition velocity. That is a governance diagnosis wearing a finance costume.

At the practice level, Governance Debt is the offer spread. When two practices with identical production receive materially different offers, the buyer is not pricing the dentistry. The buyer is pricing transferability — whether the enterprise functions as an institution or as an extension of one person's memory. Every undocumented decision pathway, every role defined by habit rather than charter, every process that lives in the owner's head is a discount, applied silently, in the only audit that ever prices these things honestly: due diligence.

The spread is your Governance Gap, denominated in dollars.

The test is already running

Here is what has changed, and why this is not an abstract argument.

With nearly four in five DSOs anticipating recapitalization within 36 months, every buyer in the market is now underwriting against the failures they just watched. "Increased scrutiny on financials, operations, and projections" is the polite phrasing. The functional question being asked in diligence is simpler:

Can this organization retrieve the controlling decision — the policy, the authority, the documentation — on any operational question, quickly, without depending on any single individual?

We call this the 60-Second Retrieval Standard, and buyers are effectively administering it whether sellers realize it or not. Organizations that pass command the top of the spread. Organizations that fail fund the bottom of it.

The 60-Second Retrieval Test:

Capital allocation authority. Regional management autonomy. Clinical escalation pathways.

For each: is the controlling decision documented architecture — or someone's memory?

Two or more on memory is unpriced Governance Debt.

The threshold

There is a reason this condition surfaces on a schedule rather than at random.

Below a certain scale, informal systems genuinely work. A founder can hold the pricing logic, the payer strategy, the personnel exceptions, and the clinical standards in memory, and proximity does the rest. This is why so many owners sincerely believe they have no governance problem — for years, they didn't. The system was the founder, and the founder was in the building.

Our research places the break point at roughly ten operating units — The 10-Unit Governance Threshold, documented in Kingsley Group's March research brief on the transition from proximity-based management to authority-based architecture. The threshold is a structural signal rather than a fixed rule: organizations dispersed across multiple states frequently encounter it earlier, often between six and eight locations, while dense single-market groups may reach it later. Past it, proximity-based management fails structurally, not gradually. A directive issued once is interpreted three ways across twelve locations. Regional managers become messengers rather than decision-makers because no one ever defined what they hold authority over. The organization begins consuming executive heroism as an operating input.

The events of the months since that brief was published have functioned as an uninvited field test.

The trap is in the diagnosis. Leaders assume growth created the complexity. It did not. The complexity was latent the entire time; growth merely exposed it — while simultaneously removing the one person who had been silently compensating for it. Organizations do not outgrow their people. They outgrow their decision systems.

This is also why the current crises land the way they do. A staffing shortage does not create chaos; it exposes organizations already dependent on undocumented judgment. AI does not add complexity; it accelerates the speed at which ungoverned decisions become visible.

Every surface, same fracture

Run the retrieval test against the crises no one connects to M&A at all and the pattern holds. Staffing churn concentrates where scope, authority, and escalation are ambiguous — pay retains people; incoherence expels them. Case acceptance collapses where treatment presentation varies by operator because no one governs the standard. And the newest exposure is the one almost no one has documented anywhere: as diagnostic AI rolls out across networks, groups are deploying tools that flag interventions without ever answering who holds decision rights when the algorithm and the clinician disagree — or what the escalation pathway is when an associate simply ignores the flag. That is not modernization. That is authority ambiguity with a liability attached.

The wrong debate

The loudest argument in dentistry right now — sell to a DSO, stay independent, build a group — assumes the outcome depends on which door you choose.

The evidence of 2026 says otherwise. The lender takeovers prove scale does not exempt an organization from governance; it multiplies the penalty. The offer spread proves independence does not exempt a practice from institutional standards; the market applies them at the moment of transfer regardless. Whichever future an owner chooses, the asset that determines the result is the same one: a decision architecture that holds under pressure, independent of any single person.

The organizations that win the next five years will not simply be the ones with more staff, better software, or cheaper capital. They will be the ones whose answers to who decides, who owns it, and where is it written survive an audit.

The market has stopped buying dentistry. It has started buying governance — or, in the language a lender would use, durability: the capacity of an organization to hold its coherence when its founder, its margins, or its luck gives out. Every operational debate now running in this industry — the AI rollout, the assisted-hygiene model, the PPO exit, the regional expansion — reduces to the same question, and it is the one dentistry forgot to ask: Who owns this decision?

Ask it in just three domains — capital allocation, regional management autonomy, clinical escalation — and time the answers. If the honest response in two or more is "it depends who you ask," the organization is carrying Governance Debt it has not priced. Kingsley Group's 10-Unit Governance Diagnostic exists to make that answer visible before a buyer, a lender, or a crisis makes it visible first.

A note on sources. Market data referenced in this analysis draws on the TUSK Practice Sales Q2 2026 Dental Market Report (buyer demand, recapitalization pipeline, offer dispersion, and diligence trends); the American Dental Association Health Policy Institute's quarterly Economic Outlook and Emerging Issues in Dentistry reports (insurance network exits, practice busyness, and staffing conditions); and 2026 trade reporting from Becker's Dental + DSO Review and Group Dentistry Now on DSO restructurings, lender transitions, and platform activity. Characterizations of specific organizations reflect published reporting as of this writing.

Kingsley Group publishes institutional governance frameworks for dental enterprises: decision rights, accountability continuity, clinical authority, and operational transferability.

The market is pricing decision architecture. Benchmark yours.

Step 1 — Quantify the gap.

The 10-Unit Governance Threshold Research Brief and Diagnostic establish where implicit authority is carrying your enterprise — and where it will be priced.

[ Request the Research Brief & Diagnostic ]Step 2 — See what the gap costs.

The $1.9M Question* — Kingsley Group's introductory analysis of governance value at transfer. $97